Solution 4.7

a) Calculate the break-even point in both sales volume and revenue

Before one can attempt this question one must classify costs into fixed and variable and calculate the contribution per person. In this question all the costs are fixed except for the commissions to the coach operators and management .

| Selling Price (5.00 x 100/113.5 to exclude vat) |

|

4.40 |

|

| Variable cost per person 4.4 x 15% |

|

0.66 |

|

| Contribution per person |

|

3.74 |

|

|

|||

| Fixed costs Operating costs | 39,500 |

||

| Loan interest | 4,800 |

44,300 |

|

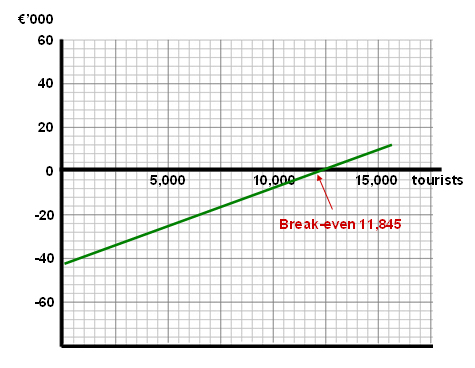

Breakeven point in units and revenue

| Fixed costs |

€44,300 |

= 11,845 persons |

| Contribution per person | €3.74 |

|

|

|

|

Units x sales price |

11,845 x €4.40 |

= €52,117 revenue |

b) If Charlie requires a profit of 10,000, what turnover must he achieve

This is calculated by using the formula

Fixed costs + Profit required = 44,300 + 10,000 = 14,519 persons

Contribution per person 3.74

In sales value this will amount to 63,883 (14,519 x 4.40)

c) If fixed costs increase by 10 per cent, calculate the level of sales Charlie will have to achieve to maintain his profit requirement

In this case fixed costs will increase to 48,730

The answer to the question is calculated using the same formula as in (b)

Fixed costs + Profit required = 48,730 + 10,000 = 15,703 persons

Contribution per person 3.74

In sales value this will amount to 69,093 (15,703 x 4.40)

d) Prepare a profit volume graph showing clearly the break-even point and the margin of safety, if he achieves his required profit.

e) Comment on the viability of the venture

At present the venture is not a viable one. To break-even requires 11,845 customers which equates with 228 visitors per week. This is very high and will just achieve break-even. The admission charge however is quire low. If this was increased to 9 including VAT (7.93 net) then the break-even point would fall to 6573 persons which is 126 per week (see below). This is a more realistic figure

The business should also consider adding in other revenue streams such as souvenir and café shop as well as possibly developing organic farm produce to sell.

|

|

|

|

|

|

|

|

|

Selling price excluding VAT = |

(9 x 100/112.5) |

7.93 |

|

|||

|

Less variance costs |

|

15% |

|

1.19 |

|

|

|

Contribution |

|

|

|

6.74 |

|

|

|

|

|

|

|

|

|

|

|

New break-even point = 44,300/6.74 = 6573 persons |

|

|

||||

|

|

|

|

|

|

|

|